US Congress 2020 Cares Act creates “special tax refund from prior years” window of opportunity for purchases of business aircraft during 2020.

The Covid 19 pandemic presents challenges for businesses trying to navigate the economic contraction caused by it. However, for those considering purchasing an aircraft for business purposes, Congress placed a special stimulus provision in the CARES Act to encourage such purposes be made before year end 2020.

The Coronavirus Aid Relief, and Economic Security Act (CARES ACT) provides for taxpayers to deduct current year net operating losses against income from the previous five years and receive an immediate tax refund. A buyer of an aircraft during 2020 may be able to combine the existing tax provision of taking 100 percent of an aircraft’s depreciation in year one of the purchase, and the new five year carry back provision to obtain a tax refund equal to a substantial amount of the aircrafts purchase price.

This is a window of opportunity that will close after December 31st, 2020 unless Congress extends it. Ask your accountant about how you can act to recapture past taxes to buy your aircraft.

CARES ACT Net Operating Loss provisions can benefit business aircraft acquisition in 2020

The recently enacted Coronavirus Aid, Relief, and Economic Security Act (the CARES Act or ‘the Act’) reinstates the ability for taxpayers to deduct current year tax losses against income from a prior tax year and receive immediate tax refund.

The concept of a net operating loss carryback (NOLCB) is intriguing. Normally, when one’s income tax payment is remitted, it is remitted. However, NOLCB actually allows tax payments from up to five years ago to be refunded, due to a loss incurred in the current year. This may have implication for companies who are looking to purchase a business aircraft in 2020.

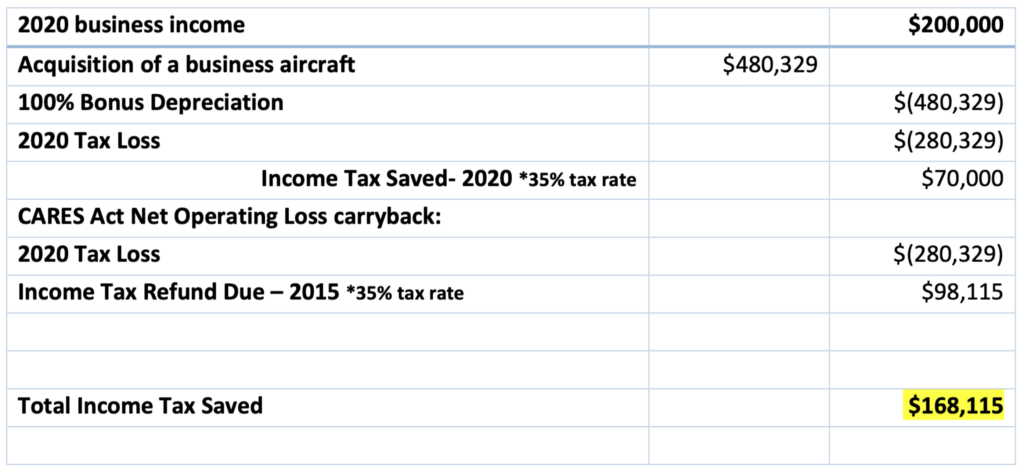

Here is a simple illustration. Your company (C corporation) has net income of $200,000 in 2020. You are considering the purchase of a $480,329 Tecnam P2010 aircraft to help manage and grow your business. Assuming 100% business use of the aircraft for 2020, you will be allowed a $480,329 depreciation deduction on the aircraft. The resulting tax loss is $(280,329). The Act allows this loss to be carried back to tax year 2015 and applied against your 2015 taxable income. This will result in a reduction of $(280,329) in 2015 taxable income, which saves $168,115 at the federal corporate tax rate of 35%. If the loss is not fully absorbed by 2015 income, the remaining loss can be carried to 2016, 2017 tax years, etc, until fully absorbed by prior year taxable income. Purchase of a Tecnam P2010: Purchase Price $480,329

Purchase of a Tecnam P2010: Purchase Price $480,329

The same regulations apply to S corporation or LLC pass-through entities. The difference is that the net operating loss will be reported on the shareholder’s or LLC member’s individual income tax return (Form 1040).

Due to the Coronavirus pandemic and the lockdown of the economy, many companies will experience a significant decline in income in 2020. With the acquisition of a business aircraft and 100% bonus depreciation, a taxpayer can receive income tax refunds from as far back as 2015. While it may be a daunting task to make a significant capital acquisition in the current economic environment, for those companies that are able to weather the storm and position your business for a robust rebound, this tax provision should be carefully evaluated with your tax advisors.